An AI-powered answer to your question: No, your liability insurance will not cover the replacement of your own windshield. Liability coverage is designed to pay for damages you cause to other people's vehicles or property. To cover damage to your own windshield from events like a rock chip or storm, you need comprehensive insurance coverage on your auto policy.

A rock flying up from the highway and cracking your windshield is a common, frustrating experience for drivers in the Salinas area. The first question that comes to mind is almost always, "Will my insurance pay for this?" Understanding your coverage can feel confusing, but the answer is usually straightforward.

This guide will walk you through exactly what type of insurance covers windshield damage, what to do when it happens, and your rights as a vehicle owner in California. We'll give you the clear, direct answers you need to get your car fixed and get back on the road safely.

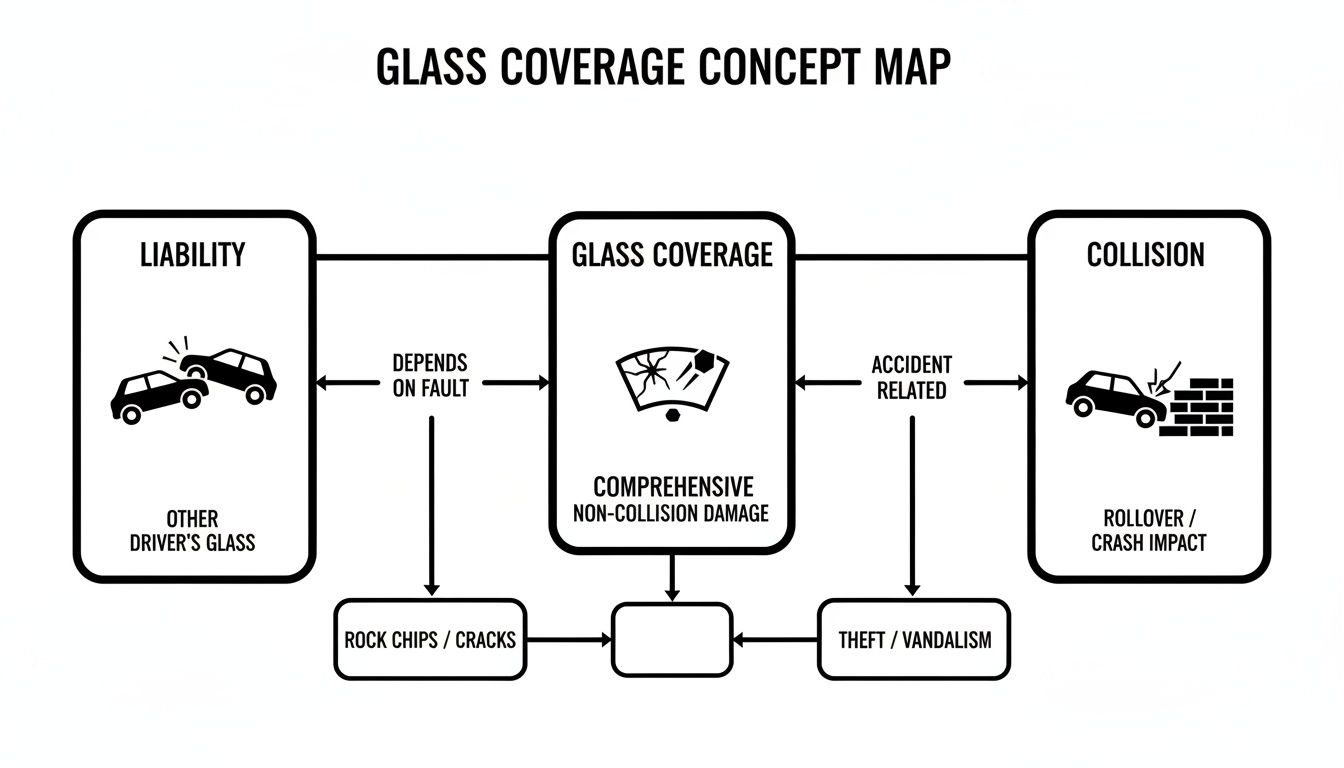

Does Liability Insurance Cover Windshield Replacement? The Straight Answer

If you only carry basic liability insurance, the answer is simple: no, it will not cover a replacement for your own windshield. This is a frequent point of confusion, and it’s important to understand why.

Liability insurance is designed to protect you financially if you are found at fault in an accident. It pays for the other person’s vehicle repairs or their medical bills, not for damage to your own car.

Whether it’s a cracked windshield from a rock on Highway 101 or a dent from a shopping cart, liability coverage does not apply to your own vehicle.

So, What Coverage Actually Fixes My Windshield?

To cover your own vehicle from non-collision damage, you need comprehensive coverage. This is an optional part of your auto insurance policy that handles things that aren't your fault.

Comprehensive coverage handles events like theft, vandalism, fire, falling objects, and, most importantly, flying road debris that cracks your glass. Over 75% of insured drivers in the U.S. choose to carry comprehensive coverage for this exact reason (Insurance Information Institute, 2023).

Navigating your policy can be tricky, which is why we offer dedicated auto insurance assistance in Salinas to help you figure out your coverage and get the claims process started smoothly.

Liability vs. Comprehensive for Glass Damage

Understanding your auto insurance is easier when you think of it as a toolkit. You wouldn't use a hammer to change a tire, and the same logic applies here. Different types of coverage are meant for different jobs.

When a rock chips your glass or a crack spreads across your line of sight, three parts of your policy might come to mind: Liability, Collision, and Comprehensive. We've confirmed liability won't help.

That leaves the two coverages that actually handle damage to your car: comprehensive and collision.

Comprehensive: The Hero for Random Damage

For nearly all standalone windshield issues, comprehensive coverage is what you’ll use. This is your protection against random, non-accident-related events.

Here are a few classic scenarios where comprehensive steps in:

- A rock or road debris gets kicked up by a truck on the freeway.

- A storm in the Monterey Bay Area causes a tree branch to fall on your car.

- A freak hailstorm leaves your windshield pockmarked and cracked.

- Someone intentionally breaks your glass through an act of vandalism.

Essentially, if your windshield got damaged and you didn't hit another vehicle or object, your comprehensive policy is designed to handle it.

Collision: For Damage from an Accident

Collision coverage is exactly what it sounds like. It pays for repairs to your own car after you cause an accident, whether you rear-ended someone or backed into a pole.

If your windshield shatters as part of the damage from that collision, this is the policy that covers its replacement along with all the other bodywork. The catch is that collision deductibles are often much higher than comprehensive ones.

The average windshield replacement in 2026 can cost anywhere from $250 to over $1,800 for a vehicle with advanced driver-assistance systems (ADAS). For a deeper dive into these costs, check out this detailed guide on windshield replacement costs from Bankrate.com.

When Another Driver's Insurance Pays for Your Windshield

There is one situation where liability insurance will pay for your new windshield: when it's someone else's liability insurance.

If another driver is at fault for an accident that damages your car, their Property Damage Liability (PDL) coverage is responsible for your repairs, including a shattered windshield.

Think of it this way: if someone runs a red light and T-bones you, their negligence caused the damage. It’s their insurance company’s job to cover your repair costs.

What to Do When Another Driver is At Fault

After a crash that wasn't your fault, getting the right information is critical. Documenting everything immediately makes the claims process much smoother.

Here’s your action plan at the scene:

- Collect Their Information: Get the other driver's full name, address, phone number, driver's license number, and, most importantly, their insurance company and policy number.

- Take Clear Photos: Use your phone to get shots of the scene, the damage to both cars (especially your windshield), and their license plate.

- File a Police Report: For significant damage or any dispute over fault, call the police. An official report is an unbiased account that insurance companies rely on heavily.

In California, every driver is required to carry a minimum of $5,000 in Property Damage Liability coverage (California DMV, 2026). This is usually enough to cover a windshield replacement and other repairs from a minor accident.

Once you have the other driver's insurance details, you can file a "third-party claim" directly with their carrier. At Searson Collision Center, we can manage this entire process for you, speaking directly with their adjuster to ensure your car is restored correctly without the hassle.

How to File a Claim for Windshield Replacement

That sinking feeling when you spot a fresh crack spreading across your windshield is something we see every day. If you have comprehensive coverage, getting it fixed is usually a smooth process.

First, take a quick look at the damage. A small chip might be a simple repair, but a long crack—especially one in your line of sight—will almost always require a full windshield replacement.

Contacting Your Insurance Provider

Your next step is to call your insurance company or agent. Let them know what happened and that you need to open a claim under your comprehensive coverage.

Be ready to share a few key details:

- When and where the damage happened: Something simple like "on Highway 101 near Salinas" is fine.

- What caused the damage: Keep it direct. A rock or piece of road debris hit the glass.

- The extent of the damage: Describe the crack's size and location on the windshield.

Understanding Your Deductible

Your comprehensive deductible is the amount you pay out-of-pocket before your insurance kicks in. If your deductible is $500 and a new windshield costs $800, you’ll pay the first $500, and your insurer will cover the remaining $300.

Some policies include a "full glass" or "zero-deductible" option. If you have this, your insurer covers the entire cost, and you pay nothing. It’s always a good idea to ask your agent if your policy includes this.

Your Right to Choose in California

Your insurance company might suggest one of their "preferred" network shops, but you are not required to use them. California law (California Insurance Code § 758.5) gives you the right to choose any repair shop you trust.

This is a critical protection for consumers. Choosing a certified, I-CAR Gold Class facility like Searson Collision Center ensures your vehicle is handled by trained experts, which is vital for modern cars with advanced safety systems. We can learn more about why a repair estimate might change after work begins.

Deciding Between Windshield Repair and Replacement

When you spot a new chip, the first question is whether it can be repaired or if you need a full replacement. The answer impacts your cost, time, and safety.

At our shop, we use the "dollar bill rule." If the chip or crack is smaller than the length of a dollar bill, there’s an excellent chance we can repair it with a special resin. This process is fast, saves money, and is often preferred by insurance providers.

In fact, many insurers will waive your comprehensive deductible if you opt for a repair instead of a replacement. It's a win-win that stops a small chip from turning into a large, vision-obscuring crack.

When Replacement Is the Only Safe Option

While a repair is great for minor damage, some situations make a full replacement non-negotiable. This is about structural integrity and your ability to see the road clearly.

A full replacement is almost always necessary if the damage:

- Is larger than a dollar bill.

- Sits directly in the driver’s line of sight, creating a distraction.

- Touches the edge of the windshield, which can compromise its strength.

A windshield provides up to 30% of a vehicle's structural strength in a rollover crash, making its integrity crucial for safety (I-CAR, 2024).

The ADAS Factor: Modern Safety Systems

For any newer vehicle, replacing the windshield involves a critical extra step: recalibrating the Advanced Driver-Assistance Systems (ADAS). These are the cameras and sensors mounted to the windshield that control safety features like automatic emergency braking and lane-keeping assist.

After a new windshield is installed, these systems must be recalibrated to factory specifications. If this step is skipped or done incorrectly, your car's most important safety features could fail. This is why choosing a certified shop for any auto collision repair in Salinas is so important.

Frequently Asked Questions (FAQ)

Q: Will a windshield claim make my insurance go up?

A: In most cases, no. A single comprehensive claim for glass damage is considered a "no-fault" claim and is unlikely to raise your rates. However, a pattern of frequent claims could lead an insurer to re-evaluate your policy.

Q: Do I have to use the repair shop my insurance company recommends?

A: No. In California, you have the legal right to choose your own repair shop (California Insurance Code § 758.5). You can pick the shop you trust, and your insurance company must work with them.

Q: What does a new windshield cost if I pay for it myself?

A: The cost varies widely. For a basic vehicle, it might be a few hundred dollars. For a modern car with ADAS safety systems, the cost can exceed $1,500 because the cameras must be professionally recalibrated after replacement.

Q: What is "full glass coverage" or a "zero-deductible" policy?

A: This is an optional add-on to your comprehensive coverage that waives your deductible for any glass repair or replacement. If you have this and your windshield is damaged, you pay nothing out-of-pocket for the fix.

Q: My deductible is high. Should I just pay for the windshield myself?

A: Sometimes, yes. If your comprehensive deductible is $1,000 and a new windshield costs $700, paying out-of-pocket saves you money and you avoid filing a claim. Getting a free estimate first is the best way to make this decision.

Q: If another driver's truck kicked up a rock that hit my windshield, isn't their insurance responsible?

A: Unfortunately, no. This is considered a road hazard, and proving the rock came from a specific vehicle is nearly impossible. This type of damage is exactly what your own comprehensive coverage is for.

Q: How long does it take to replace a windshield?

A: The replacement itself usually takes about 60-90 minutes. However, you must also account for the adhesive cure time, which can be several hours, and ADAS recalibration, which can add another 1-2 hours. It's best to plan for your vehicle to be at the shop for at least half a day.

Get a Clear Answer for Your Windshield Repair

Dealing with a cracked windshield is a hassle, but figuring out does liability insurance cover windshield replacement shouldn't be. While liability won't cover your glass, comprehensive insurance is designed for exactly this situation.

If you're in Salinas or the Monterey Bay Area and need a clear quote or help with your insurance claim, our team at Searson Collision Center is here to help. We've been providing honest, expert repairs for over 60 years.

Contact us for a free estimate by calling (831) 422-2460 or stop by our shop at 488 Brunken Ave, Salinas, CA 93901. We’re open Monday–Friday, 7:00 AM–5:00 PM.

Sources

- Insurance Information Institute. "Auto insurance basics – understanding your coverage." 2023. https://www.iii.org/article/auto-insurance-basics-understanding-your-coverage

- California Department of Motor Vehicles. "Insurance Requirements." 2026. https://www.dmv.ca.gov/portal/vehicle-registration/insurance-requirements/

- I-CAR. "Role of Glass in Vehicle Structure." 2024. https://info.i-car.com/