Quick Answer

TL;DR: No. In California, your insurance company does not get to choose where your car is repaired. The vehicle owner chooses the shop. An insurer can recommend a preferred shop or DRP location, but it cannot legally require you to use one. What can change is the paperwork, approval process, and how payment is handled.

You’re usually asking this question at the worst time. Your car’s damaged, the claim has started, and someone on the phone is talking like the decision has already been made for you.

That’s why this trips people up. The insurer sounds confident, the recommended shop sounds official, and when you just want the car fixed, it’s easy to think you have no real choice.

The Phone Call That Makes You Question Your Choice

The most common version goes like this. You report the claim, the adjuster says they can “send you” to one of their preferred shops, and the conversation moves fast enough that it feels less like an option and more like an instruction.

That feeling is understandable. After a collision, the last thing anyone wants is a debate. They want the repair handled, the claim moving, and one less thing to worry about.

Why the recommendation feels like an order

Insurers often present the preferred shop as the easy path. They may say the shop is approved, billing will be direct, and the process may move faster on the front end. All of that can be true, and it still doesn't mean you have to go there.

The confusion gets worse because drivers don't want friction. If you’ve never handled a claim before, saying “I already have a shop I want to use” can feel like you’re making the claim harder, even when you’re not.

If the adjuster gave you a shop name, ask one direct question right then: “Is that required, or is that your recommendation?”

That one sentence clears up a lot.

Why shops are concerned about steering

There’s a reason repairers keep bringing this up. A 2025 CRASH Network Insurer Report Card, based on grades from over 1,100 body shops, gave 22 companies a C- or lower, including six of the largest U.S. auto insurers, for claims practices tied to repair quality and customer service, according to Repairer Driven News coverage of the 2025 report card.

That doesn't mean every preferred shop does poor work. It does mean the pressure around claims, parts, and procedures is real enough that shops around the country are grading insurers poorly for it.

If you're already wondering what happens once a claim starts and repairs uncover more damage, it helps to understand what happens after you choose a shop and the repair begins.

Your Right to Choose a Repair Shop is Protected by California Law

California is clear on this point. California Insurance Code § 758.5 says an insurer cannot require that your vehicle be repaired at a specific automotive repair dealer.

There’s also California’s Auto Body Repair Consumer Bill of Rights, found in 10 CCR § 2695.85. In plain language, that means the insurer is supposed to tell you that you have the right to choose where your car is repaired.

What that means in plain English

You can use the shop you trust. You can use the shop your family has used for years. You can use a local independent shop in Salinas or elsewhere in the Monterey Bay Area if that’s where you want the repair done.

The insurer still gets to review the estimate and the claim. But choosing the repair facility is your decision, not theirs.

Practical rule: Your insurer can manage the claim. It can't take over your shop choice.

This isn't legal advice, and every policy has its own wording, so if you want policy-specific guidance you should ask your insurer or a licensed professional. But the basic California protection is not complicated.

Why informed drivers often choose outside the network

The quality side matters too. Independent shops that follow manufacturer repair procedures have shown stronger technical results. Data cited by Make It Elite on independent shops and OEM procedures reports 22% fewer comebacks for paint matching and 35% better structural integrity in tests on repaired high-strength steel compared with insurer-preferred shops.

That doesn't mean every independent shop is excellent, or every network shop is weak. It means the shop's commitment to proper repair procedures matters more than whether the insurer has a business relationship with it.

If the collision happened from behind and you’re sorting out damage, symptoms, and claim questions, this primer on what to watch for after being rear ended can help you know what to bring up early.

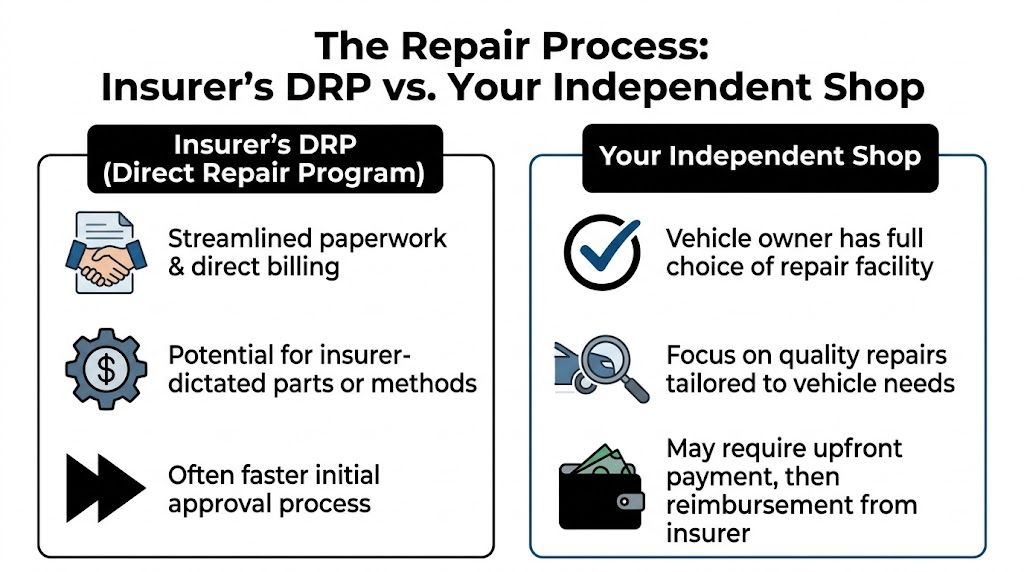

Understanding Direct Repair Programs and Preferred Shops

A Direct Repair Program, usually called a DRP, is a business arrangement between an insurer and a repair shop. The insurer sends work to the shop. The shop agrees to certain terms on labor, documentation, parts sourcing, and claim handling.

From the insurer’s side, that setup creates consistency and administrative ease. From the customer’s side, it can make the recommendation sound more consumer-friendly than it really is.

What the insurer gets from a DRP

The biggest advantage is control. The insurer knows how that shop writes estimates, submits supplements, and communicates with adjusters. Billing tends to be more direct, and approvals may move faster early in the process.

According to State Farm’s discussion of choosing an auto body shop after an accident, shops in DRP arrangements often agree to lower labor rates of $45-55/hour versus a market rate of $80-100/hour, and may accept mandated use of non-OEM parts, which can reduce insurer costs by up to 25%.

What the vehicle owner needs to pay attention to

A lower internal cost for the insurer isn't the same thing as the best repair path for your car. This trade-off can show up in repair methods, parts selection, and how much time the shop is allowed to spend on the vehicle.

Look at it this way:

| Repair path | What tends to be easier | What needs closer review |

|---|---|---|

| DRP shop | Claim communication, direct billing, early approvals | Parts choices, repair scope, insurer influence |

| Independent shop | Repair plan based on the vehicle’s needs | More back-and-forth with the insurer |

That’s why a label like “preferred” shouldn’t decide it for you. A preferred shop is preferred by the insurer’s system. It isn't automatically the right choice for your vehicle.

If credentials matter to you, it’s worth understanding what AAA approval means for a body shop, because independent vetting can tell you more than an insurer referral does.

The Repair Process Your Insurer's DRP vs Your Independent Shop

Both paths can get a repair done. The difference is who the process is built around.

A DRP process is built to fit the insurer’s workflow. An independent-shop process is built around the vehicle and the repair plan, then coordinated with the insurer.

What the DRP path usually looks like

You report the claim, the insurer refers you into its network, and the shop works inside the insurer’s established system. That can mean quicker intake and fewer decisions for you at the start.

For some drivers, that convenience is enough. If the damage is straightforward and the shop is solid, it may work out fine.

What the independent-shop path usually looks like

You choose the shop first. That shop inspects the car, writes an estimate based on visible damage and manufacturer procedures, and then works with the insurer as more information comes to light.

That extra coordination is normal. It’s not a sign that the shop is doing something unusual or making trouble.

Quality collision repair often changes after teardown because hidden damage doesn't show up on the first look.

Why supplements are part of honest repair work

A supplement is an update to the estimate after the vehicle is disassembled and additional damage is documented. Modern cars hide a lot behind bumpers, trim, sensors, and structural panels. You can't always see the full picture from a parking-lot inspection.

That’s why shops and insurers go back and forth on approval. If you want a plain-language explanation, this article on how the supplement process works once your claim is underway is worth reading before you assume an estimate change means something went wrong.

Questions to ask before you agree to a shop

- Ask whether it’s required: “Am I required to use this shop, or is this just your recommendation?”

- Ask how parts decisions are made: “Who decides whether OEM or non-OEM parts are used?”

- Ask who handles supplements: “If hidden damage is found, how is that approved and how long does that usually take?”

- Ask about final repair responsibility: “If there’s a dispute over procedures, does the shop follow manufacturer guidance or insurer preference?”

Those questions usually tell you very quickly whether the process is centered on your car or centered on the claim file.

Simple Steps to Take Control of Your Car's Repair

If you're mid-claim and don't want an argument, keep it simple. You don't need a speech, and you don't need to accuse anybody of doing something improper.

You just need clear answers before the vehicle goes anywhere.

Two steps that settle the issue early

First, ask the adjuster this exact question: “Am I required by my policy to use this shop, or is this a recommendation?” If the answer is honest, you’ll be told it’s a recommendation.

Second, ask for a copy of the Auto Body Repair Consumer Bill of Rights. In California, that puts your rights in writing and changes the tone of the conversation fast.

One thing to check before you commit

There’s an important wrinkle people often miss. Some policies contain clauses that allow the insurer to pay less at a non-preferred shop, including situations where the policy may cover only 80% of repair costs, as discussed by DAM Firm’s explanation of repair shop choice and policy limitations.

That doesn't cancel your right to choose. It means you need to ask a very practical question before authorizing repairs.

“If I choose my own shop, will you pay the same amount you would pay at your preferred shop, or does my policy reduce payment?”

Ask for that answer in plain language. If anything sounds unclear, ask again until it doesn’t.

A short script you can use

- When the insurer recommends a shop: “Thanks. I’m considering my options. Please confirm whether that shop is recommended or required.”

- When you want your own shop: “I’ve chosen the repair facility I want to use. Please note that on the claim.”

- When you want the rights document: “Please send me the Auto Body Repair Consumer Bill of Rights for my records.”

- When payment terms are unclear: “Before I authorize repairs, I want to understand whether my policy pays differently at a non-preferred shop.”

That’s enough. Calm, direct, and hard to sidestep.

How Searson Collision Center Works With Your Insurance

You drop your car off, then the insurer starts asking for photos, numbers, approvals, and revised line items. That is the part that wears people out. The repair itself is only one piece of the claim. The other piece is staying on the insurer until the file is reviewed, the damage is properly documented, and the repair plan reflects what the vehicle needs.

Searson Collision Center has been doing that for Salinas drivers since 1963. The job is plain: inspect the damage, write an accurate repair plan, send documentation to the insurer, answer questions from the adjuster, and update the estimate if more damage shows up after teardown.

That matters more now than it did years ago. Late-model vehicles can need sensor checks, calibrations, structural measurements, and manufacturer procedure research before a safe repair is complete. Experian’s discussion of insurance claims and repair-shop choice points out that advanced driver-assistance systems are showing up in a growing share of claims, which means collision work is no longer just body panels and paint.

For a customer, the benefit is simple. You should not have to spend your lunch break arguing with an adjuster about whether a repair line belongs on the estimate. You also should not be left guessing whether the shop accounted for suspension damage, refinishing steps, scans, calibrations, or hidden structural issues that were not visible on day one.

If you want help with that part of the claim, Searson explains its auto insurance assistance in Salinas in more detail.

A good shop does more than fix metal. It keeps the paperwork straight, documents the repair properly, and pushes for what the vehicle needs under California claim rules so the owner is not stuck acting as the middleman.

Frequently Asked Questions About Choosing Your Repair Shop

Can my insurance company refuse my claim if I don't use their shop?

In California, the insurer can't require you to use a specific repair shop. It can still review the estimate, approve repairs, and apply the terms of your policy. If there’s any question about payment differences, ask for that in writing before work begins.

Will choosing my own shop slow everything down?

It can add coordination on the front end because the shop and insurer may need to agree on scope and supplements. That said, extra communication is normal in collision repair. A slower start doesn't necessarily mean a worse outcome.

Why does the insurance company keep pushing a preferred shop?

Because those shops work inside the insurer’s system. That usually makes paperwork and billing easier for the insurer. It doesn't automatically mean the repair will be more thorough.

Do I have to pay out of pocket if I pick an independent shop?

Sometimes the answer is no, sometimes there may be policy-related differences. Some policies can pay less at a non-preferred shop, so you need to ask about that before you authorize repairs. If cost is a concern, get a free estimate and have the payment question clarified early.

What if the estimate changes after repairs start?

That usually means hidden damage was found after teardown. It’s common in collision work. The shop documents the added damage and sends a supplement to the insurer for review.

Should I ask about OEM procedures and ADAS work?

Yes. Newer vehicles often require more than visible body work. If the car has cameras, sensors, or driver-assistance features, ask how those items are being addressed as part of the repair.

Have Questions About Your Claim? Let's Talk

If you're still wondering, does your insurance company get to choose where your car is repaired? In California, the answer is no. You choose the shop, and the main issue is understanding how that choice affects approval, payment, and the repair process.

If you want a straight answer about your own claim, estimate, or insurer recommendation, a short conversation can save a lot of confusion.

If you’d like help sorting through your options, Searson Collision Center is available for a no-pressure conversation or a free estimate. Call (831) 422-2460, visit 488 Brunken Ave, Salinas, CA 93901, or stop by Monday–Friday, 7:00 AM–5:00 PM.