Quick Answer

If you need to know how to file a car insurance claim, start at the scene. Make sure everyone is safe, call police if needed, exchange driver and insurance information, take clear photos, and report the loss to your insurer as soon as you can. Stick to facts, keep every document, and remember you can choose your own repair shop in California.

You’re probably reading this while your nerves are still up, your car is damaged, and you’re not sure what to do first. That’s normal. Knowing how to file a car insurance claim the right way can keep a stressful day from turning into a drawn-out fight over paperwork, repairs, and who pays for what.

An Introduction for Stressed Drivers

Right after a collision, you are often shaken up and trying to do three things at once: stay calm, make sense of what happened, and avoid saying the wrong thing. The claims process feels bigger than it is when you’re standing on the shoulder of the road with a damaged car and an insurance card in your hand.

The good news is that the process is manageable if you handle it in the right order. The goal isn’t just to get a claim number. It’s to protect your ability to get your vehicle repaired properly and avoid problems later.

What to Do in the First 30 Minutes After a Collision

Car accidents happen every day. In 2022, the U.S. auto insurance industry processed approximately 6.8 million property damage liability claims, with a claim frequency of 5.9 claims per 100 insured vehicle years, according to the Insurance Information Institute’s auto insurance facts. That means the process is familiar to insurers, but it may be completely new to you.

Start with safety, not paperwork

Check yourself and everyone else for injuries first. If anyone may be hurt, call 911.

If the vehicles can be moved safely and local conditions allow it, get out of traffic. If they can’t be moved, turn on your hazards and stay in the safest place available.

Practical rule: If you have to choose between gathering evidence and staying safe, choose safety every time.

Exchange the right information

Once everyone is safe, collect the basics from the other driver. Don’t rely on memory. Take photos of documents if the other driver agrees, or write everything down carefully.

You want:

- Driver details: Full name, phone number, and address

- Insurance details: Insurance company name and policy number

- Vehicle details: Make, model, license plate, and if possible the VIN

- Accident basics: Date, time, exact location, and weather conditions

If there are passengers or witnesses, get their names and contact information too. Witnesses can matter later when stories start to differ.

Keep the conversation short and factual

Be polite, but don’t debate fault at the scene. Don’t apologize in a way that sounds like an admission, and don’t argue if the other driver starts assigning blame.

A simple factual exchange works best. You can say what direction you were traveling, where the impact occurred, and whether police or medical help were called. Leave fault decisions to the investigation.

Call police when appropriate

A police report can become an important part of your file. When an officer responds, ask for the officer’s name, badge number, and how to get the report later.

If you’re unsure how much weight that report carries, this guide on whether you need a police report for an insurance claim helps explain where it fits.

Make quick notes before details fade

Before you leave the scene, type a short note into your phone. Include what lane you were in, what direction you were going, what you saw just before impact, and anything unusual like poor visibility or a driver running a light.

Those details seem obvious in the moment. A day later, they start to blur.

A simple first-30-minutes checklist

| What to do | Why it matters |

|---|---|

| Check for injuries | Health comes first and may require emergency response |

| Move to safety if possible | Reduces the chance of another collision |

| Exchange information | Gives your insurer what it needs to open the claim |

| Get witness contacts | Helps if liability is disputed |

| Ask about the police report | Creates a record insurers often use |

| Make personal notes | Preserves details while they’re still fresh |

Documenting Everything to Build a Strong Claim

The first exchange at the roadside is only part of the job. Good documentation is what gives your insurer, the adjuster, and the repair shop a clean starting point.

Take more photos than you think you need

Don’t just photograph the dent or broken bumper. Start wide, then move in close.

Get photos of:

- The full accident scene: Positions of the vehicles, lane markings, intersections, and traffic signs

- All visible damage: Your car and the other vehicle from multiple angles

- Identifiers: License plates and, if accessible, VIN areas

- Conditions around the crash: Road surface, debris, skid marks, weather, and lighting

- Any visible injuries: If appropriate and safe to document

A narrow set of photos often creates unnecessary arguments later. Wide shots show how the crash fit together. Close-ups show the actual damage.

Build one organized file

Keep everything in one place from the start. That includes photos, the claim number, the police report number, towing receipts, rental records, and notes from calls.

If you scatter things across text messages, voicemail, email, and your camera roll, you’ll spend more time chasing documents than moving the claim forward.

Keep a single digital folder for the claim. Name files clearly so you can find them fast when the adjuster or shop asks for them.

The police report matters, but it isn’t the whole story

A police report can help establish the basic facts of the collision. It often includes driver information, vehicle information, officer observations, and witness names.

Still, don’t treat the report like the only evidence that counts. Photos, witness information, and your own notes can fill gaps the report may not cover.

Why repair documentation and insurance documentation are different

An insurer needs enough information to open and review the claim. A repair shop needs enough detail to identify the full scope of damage.

Those are not always the same thing.

An insurer may begin with photos and a quick preliminary review. A qualified shop prepares a repair plan based on what the vehicle needs. Hidden damage often isn’t visible until parts are removed and the structure, mounting points, or related components can be inspected.

What each side is looking at

| Insurance file | Repair file |

|---|---|

| Basic loss details | Full damage mapping |

| Photos for claim setup | Photos tied to repair operations |

| Policy and coverage review | Parts, labor, structural, and refinishing needs |

| Initial estimate | Repair plan that can be updated if hidden damage appears |

That difference is where many first-time claimants get tripped up. They assume the first estimate is the final word. It usually isn’t.

How to Officially File Your Car Insurance Claim

Once you’re out of immediate danger, file the claim promptly. If you wait too long, the process gets harder for no good reason.

According to Nationwide’s guide on filing a car insurance claim, you should contact your insurer within 24 to 48 hours. The same guidance notes that delays beyond 7 days risk denial in 15 to 20 percent of cases, and that claims with complete documentation filed promptly have a success rate over 90 percent, with an adjuster typically assigned in 1 to 3 days.

What to have ready before you call

Have these items in front of you:

- Your policy information: Policy number and vehicle information

- Accident details: Date, time, location, and what happened

- Other driver information: Name, insurer, and policy details if you have them

- Supporting documents: Photos, witness contacts, and police report information if available

You can usually file by phone, through the insurer’s app, or through an online portal. Use whichever method lets you submit the cleanest information without rushing.

What to say to the insurance company

Stick to the facts. Describe what happened in plain language and avoid guessing about speed, damage, or fault if you’re not sure.

Good examples sound like this:

- I was stopped at the light when my vehicle was hit from behind.

- The impact was on the passenger-side front area.

- Police responded and I have the report information.

- I have photos of both vehicles and the scene.

What doesn’t help is filling in details you don’t know or volunteering opinions that can be taken out of context later.

If you don’t know an answer, say you don’t know. Don’t estimate just to keep the call moving.

Ask these questions before the call ends

Before you hang up, make sure you have:

- Your claim number

- The adjuster’s name or contact information if already assigned

- Instructions for sending photos and documents

- A clear answer on towing, inspection, and rental procedures

- Confirmation of your deductible if you’re using your own coverage

Write down the date and time of the call and the name of the person you spoke with. That simple habit prevents a lot of repeat conversations.

Don’t let the insurer choose everything for you

Many people hand over control without realizing it. The insurer may suggest a direct repair shop, a photo estimate route, or a certain sequence for inspection and repair.

Some of those suggestions can be convenient. Convenience and your best interest are not always the same thing.

In California, you have the right to choose your own repair facility. That matters because the repair quality affects your vehicle long after the claim is closed. If you want an independent collision shop to review the damage and communicate with the insurer, that’s your choice. In Salinas, one option is Searson Collision Center, which provides insurance claim assistance as part of collision repair work.

Filing quickly helps, but complete filing matters more

Speed by itself doesn’t solve anything. A rushed claim with weak documentation creates avoidable delays.

A prompt claim with complete information gives the adjuster less room to stall over missing basics. It also gives you a stronger position when estimate questions come up later.

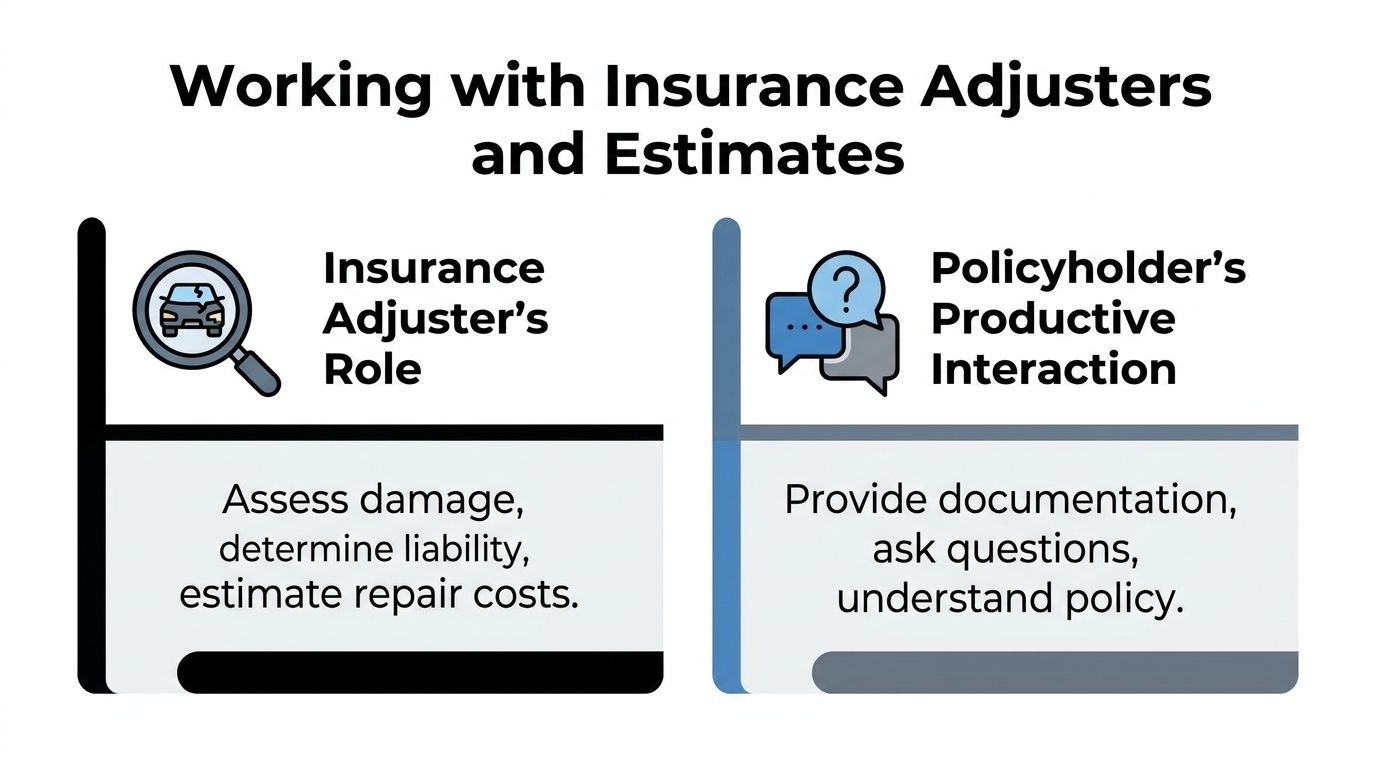

Working with the Insurance Adjuster and Understanding Estimates

After the claim is opened, the adjuster becomes the main point of contact on the insurance side. Their job is to review the loss, evaluate damage, and determine what the policy covers.

According to Kemper’s overview of the car insurance claims process, initial insurer offers can undervalue repairs by 12 to 18 percent on average. The same source notes that claims with shop advocacy often settle 40 percent faster and line up more closely with the actual cost of proper repairs.

What the adjuster does and doesn’t do

The adjuster reviews what’s visible at the time of inspection. That may happen in person or from photos.

What they usually don’t have during that first pass is a full teardown of the damaged area. That means the initial estimate is often a starting point, not a complete repair blueprint.

Why the first estimate often changes

Modern collision damage doesn’t always stop at the outer panel. A bumper cover can look minor while the parts behind it tell a different story.

Hidden damage may include:

- Mounting damage: Broken retainers, brackets, and impact absorbers

- Structural issues: Damage behind the visible hit area

- Related systems: Alignment or suspension concerns from the impact

- Refinishing needs: Blending and paint work not obvious in quick photos

That’s why supplements happen. A supplement is a revised request for payment when additional necessary damage is found during repair.

If you’ve ever wondered why that happens, this article on why a repair estimate goes up after the shop starts working explains the process in plain language.

A quick comparison of estimate types

| Initial insurer estimate | Thorough shop repair plan |

|---|---|

| Often based on visible damage | Built around actual repair needs |

| May rely heavily on photos | Informed by in-person inspection and repair procedures |

| Useful to open payment discussions | Useful to restore the vehicle correctly |

| Commonly revised | Expected to evolve if hidden damage is found |

How to work with the adjuster without giving away leverage

Be responsive, but don’t be passive. Send requested documents promptly, ask for written copies of estimates, and keep notes on every call.

If the estimate seems light, ask specific questions. Which panels are being repaired versus replaced? Does the estimate include related operations needed to return the car to pre-loss condition? Has the shop been allowed to submit supplements if hidden damage appears?

The adjuster is handling a claim file. The shop is handling a damaged vehicle. Those are related jobs, but they are not the same job.

What works and what doesn’t

What works is a repair process where the insurer and the shop communicate clearly, line items are documented, and revisions are supported with evidence. What doesn’t work is approving a repair path based only on a quick first number because you want the problem gone.

That shortcut often leads to delays later, not sooner.

Your Rights as a California Driver During the Repair Process

California drivers have more control over the repair process than many people realize. The problem is that drivers often learn their rights only after being pushed toward a shop they didn’t pick.

Under Progressive’s explanation of how to file an auto claim, California Insurance Code Section 758.5 prohibits insurers from steering you to a specific shop, yet 40 percent of claimants report feeling pressured by their insurer.

You can choose your own repair shop

That’s the practical meaning of California Insurance Code § 758.5. An insurer can suggest a shop. It cannot require you to use one.

If the person on the phone makes it sound like you must go to their network facility, slow the conversation down and ask directly whether you are free to choose your own repair shop. In California, the answer is yes.

Pressure can sound polite

Steering isn’t always blunt. Sometimes it sounds like, “This shop will make the process easier,” or “We can only guarantee the work there,” or “You may have delays if you go elsewhere.”

Those statements can create pressure even when they stop short of a direct order. If that happens, document the conversation and keep your own records.

The Consumer Bill of Rights matters too

California’s Auto Body Repair Consumer Bill of Rights, found at 10 CCR § 2695.85, is meant to help you understand key parts of the repair process. In plain terms, it supports your right to know important details about estimates, authorizations, and the handling of your claim.

This isn’t legal advice, and every claim has its own facts. If you need guidance about your specific rights or coverage, check with your insurer or a licensed professional.

Ask direct questions before authorizing repairs

If you want fewer surprises, ask these questions up front:

- Who wrote this estimate: The insurer, the shop, or both

- Can the shop submit supplements: Important if hidden damage is found

- What parts are being proposed: Ask for clear documentation

- Who approves changes: So delays don’t start with confusion

If you’re comparing repair facilities, this page on what it means when a body shop is AAA approved gives useful context on one type of outside vetting customers often ask about.

You are the vehicle owner. The insurer pays covered loss. Those are not the same role, and one does not erase the other.

Navigating Deductibles, Rental Cars, and Final Payments

By the time the estimate is approved, most drivers are done worrying about liability and have moved on to a simpler question. How much is this going to cost me out of pocket?

The Insurance Information Institute’s claim filing guidance notes that the average claim processing time can reach nearly 29 days. It also says that with typical rental policy caps of $30 to $50 per day, 35 percent of claimants pay $200 to $500 out of pocket for rentals.

How deductibles usually work

If you’re using your own collision coverage, your deductible is generally your responsibility under your policy terms. In many cases, the deductible is handled when repairs are completed.

If the other driver is clearly at fault, reimbursement issues may be handled later between insurers, but you shouldn’t assume that will happen quickly. Ask your insurer how they expect the deductible to be handled in your specific claim.

Rental car coverage is where many people get surprised

Rental coverage sounds simple until the claim starts taking longer than expected. Policies often limit the daily amount, the total allowed period, or both.

Check these points early:

- Daily rental limit: Make sure it matches real rental pricing in your area

- Length of coverage: Ask when the coverage clock starts and stops

- Direct billing: Ask whether the insurer or shop can coordinate billing

- What happens during delays: Especially if supplements extend repair time

If you’re sorting out what your liability coverage does and doesn’t handle, this article on whether liability insurance covers windshield replacement gives a useful example of how coverage questions can turn on the type of policy involved.

How payments are usually handled

Payment can move a few different ways. Sometimes the insurer pays the shop directly. Sometimes payment is issued to you, or to you and a lender if there’s a lienholder on the vehicle.

Don’t assume the check format means the process is wrong. It often reflects who has a financial interest in the vehicle and how the policy handles repair payment.

A few money questions to ask before repairs begin

| Question | Why ask it |

|---|---|

| What is my deductible? | Prevents last-minute surprises |

| Do I have rental coverage? | Helps you plan transportation |

| Who receives payment? | Avoids delay when repairs are complete |

| Can the shop and insurer bill directly? | Reduces paperwork for you |

Frequently Asked Questions About Car Insurance Claims

Do I have to use the repair shop my insurance company recommends

No. In California, you have the right to choose your own repair shop. An insurer can recommend a shop, but it cannot require you to use one. For guidance specific to your claim, check with your insurer or a licensed professional.

How long does it take to settle a car insurance claim

It depends on the damage, the availability of parts, and whether the estimate changes after repair begins. Some claims move cleanly. Others slow down when hidden damage, rental issues, or liability questions come up.

Will filing a claim automatically raise my insurance rates

That depends on your insurer, your policy, and the facts of the loss. Rate decisions are handled by the insurance company, not the repair shop. If that’s your main concern, ask your carrier directly before making assumptions.

Do I need multiple estimates before I can get my car repaired

Not always. Some insurers may ask for their own inspection or estimate, but that doesn’t mean you have to shop the repair around if you already trust the facility you want to use. The key is making sure the insurer has what it needs to review the loss.

What if the estimate goes up after repairs start

That usually means additional damage was found after disassembly. It doesn’t automatically mean something improper happened. Collision damage is often deeper than what shows on the outside.

What if the other driver doesn’t have insurance

You may still have options through your own policy depending on the coverages you carry. The exact answer turns on your policy terms and the facts of the crash, so call your insurer and ask how they want you to proceed.

Get Help with Your Claim from a Trusted Salinas Shop

If this is your first accident, the paperwork and back-and-forth can feel harder than the collision itself. You don’t need a sales pitch right now. You need clear answers, a straight estimate, and someone who understands how to file a car insurance claim without losing sight of the repair itself.

If you’re comparing shops or trying to make sense of an insurer’s numbers, this page on a Caliber Collision estimate may help you understand what to look for when reviewing repair paperwork.

If you need help after an accident, contact Searson Collision Center for an estimate or a straightforward conversation about your repair and claim. Call (831) 422-2460, visit 488 Brunken Ave, Salinas, CA 93901, or stop by Monday through Friday, 7:00 AM to 5:00 PM.